.png)

Do Kwon, the once‑celebrated founder of Terraform Labs, has been sentenced to 15 years in a US federal prison for fraud tied to the spectacular 2022 collapse of the TerraUSD (UST) and Luna ecosystem, an event that erased tens of billions of dollars in market value and shook confidence in crypto worldwide (1). His downfall, and the legal reckoning that followed, have turned Terra Luna into a case study in how fragile “algorithmic” stablecoins can be when hype outruns sound design and transparent risk management.

From “crypto visionary” to convicted fraudster

In December 2025, a US federal judge handed Kwon a 15‑year sentence after he pleaded guilty to charges including conspiracy to defraud and wire fraud, concluding a multiyear saga that began when Terra imploded in May 2022 (2). Prosecutors argued that Kwon repeatedly misled investors about how TerraUSD maintained its one‑dollar peg and concealed the true risks of his experimental system, while the judge described the scheme as an “epic” fraud that caused unprecedented damage for a crypto project.

The collapse of Terra destroyed an estimated 40 to 50 billion dollars in value in a matter of days, rippling through exchanges, lenders, and hedge funds that had built strategies around UST and Luna. Kwon fled jurisdictions and was later arrested abroad before being extradited to face US charges, and he still faces potential legal proceedings in South Korea after serving part of his sentence (3).

What Terra and Luna were meant to be

Terraform Labs launched the Terra blockchain in 2018, pitching it as an ecosystem for programmable money and payments built around a family of stablecoins, most notably TerraUSD. TerraUSD, or UST, was marketed as a crypto‑native stablecoin designed to hold a steady value of one US dollar without relying on traditional reserves such as bank deposits or Treasuries (4).

At the heart of the system sat Luna, Terra’s volatile native token, which served as a governance asset and a kind of shock absorber for UST. Luna’s market value and supply were meant to expand and contract dynamically as traders swapped between UST and Luna, creating a self‑correcting mechanism that would supposedly keep the stablecoin anchored at one dollar.

The algorithmic stablecoin mechanism

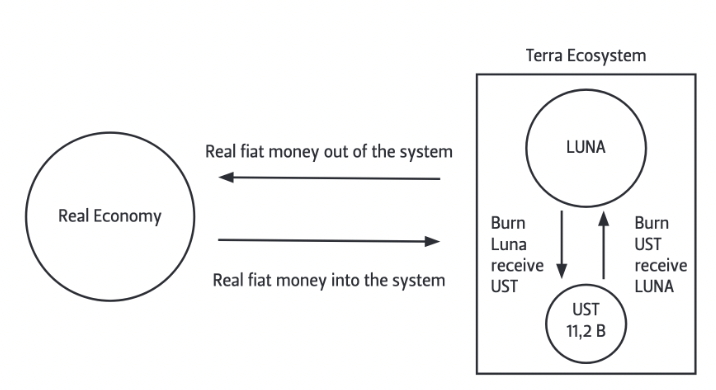

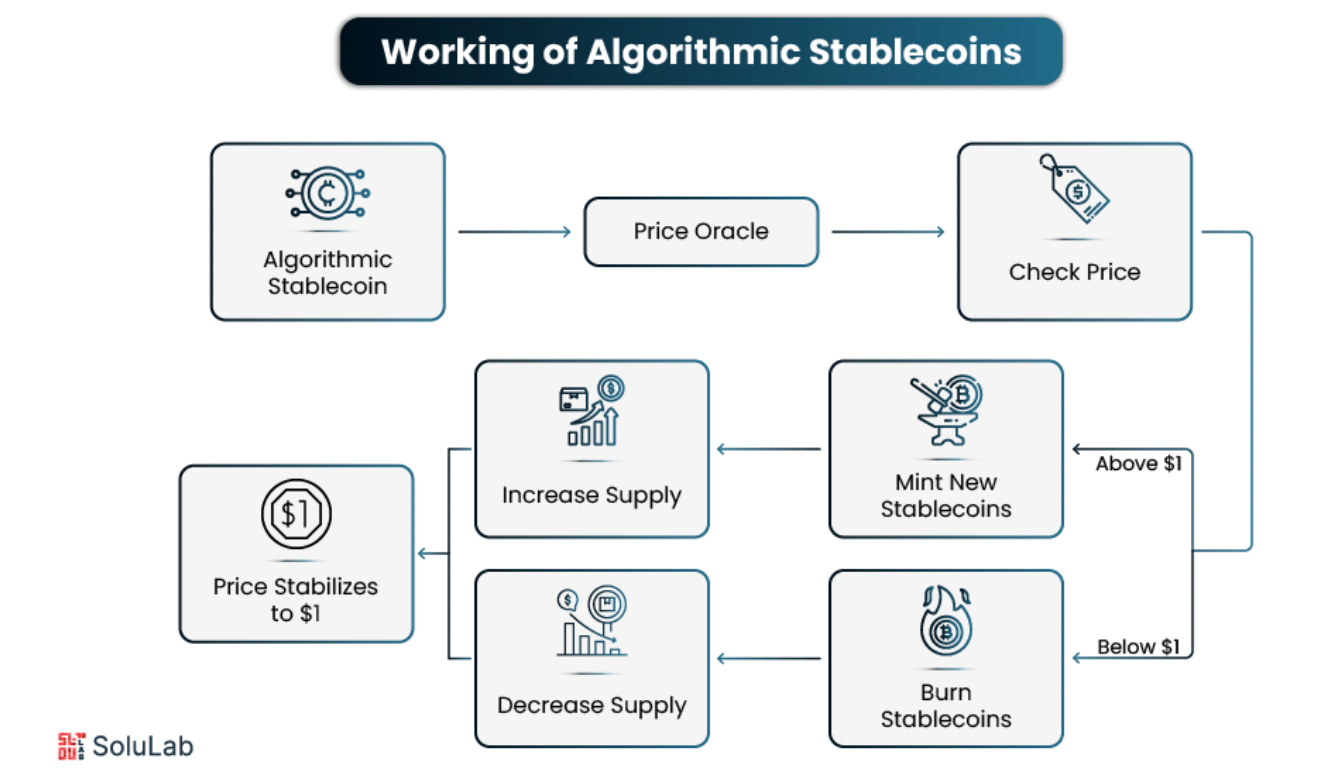

Unlike reserve‑backed stablecoins, UST relied on an arbitrage process rather than a pool of real‑world assets. The protocol allowed users to exchange 1 UST for 1 dollar worth of Luna, and vice versa, with the system minting or burning tokens to facilitate those swaps and adjust supply.

In theory, if UST fell below one dollar, traders could buy it cheaply, redeem it for one dollar of Luna, and sell the Luna, profiting from the difference and pushing UST back toward its peg. This design depended critically on market confidence and a healthy Luna price: as long as investors believed in Terra’s future and Luna stayed valuable, the arbitrage loop could appear to work as advertised (5).

High yields and rapid growth

Terra’s growth surged thanks in large part to Anchor, a lending protocol on the Terra blockchain that promised depositors unusually high yields, often around 20% on UST holdings. These yields, funded by subsidies and incentives, attracted enormous inflows from retail and institutional investors seeking stable, high returns in a low‑rate world (6).

By early 2022, UST had grown into one of the largest stablecoins, and Luna had climbed into the top tier of cryptocurrencies by market capitalization. For many, Terra looked like the flagship of an emerging alternative financial system; in reality, the ecosystem was deeply exposed to a confidence shock, because the high yields and algorithmic peg masked structural fragilities.

The depeg and death spiral

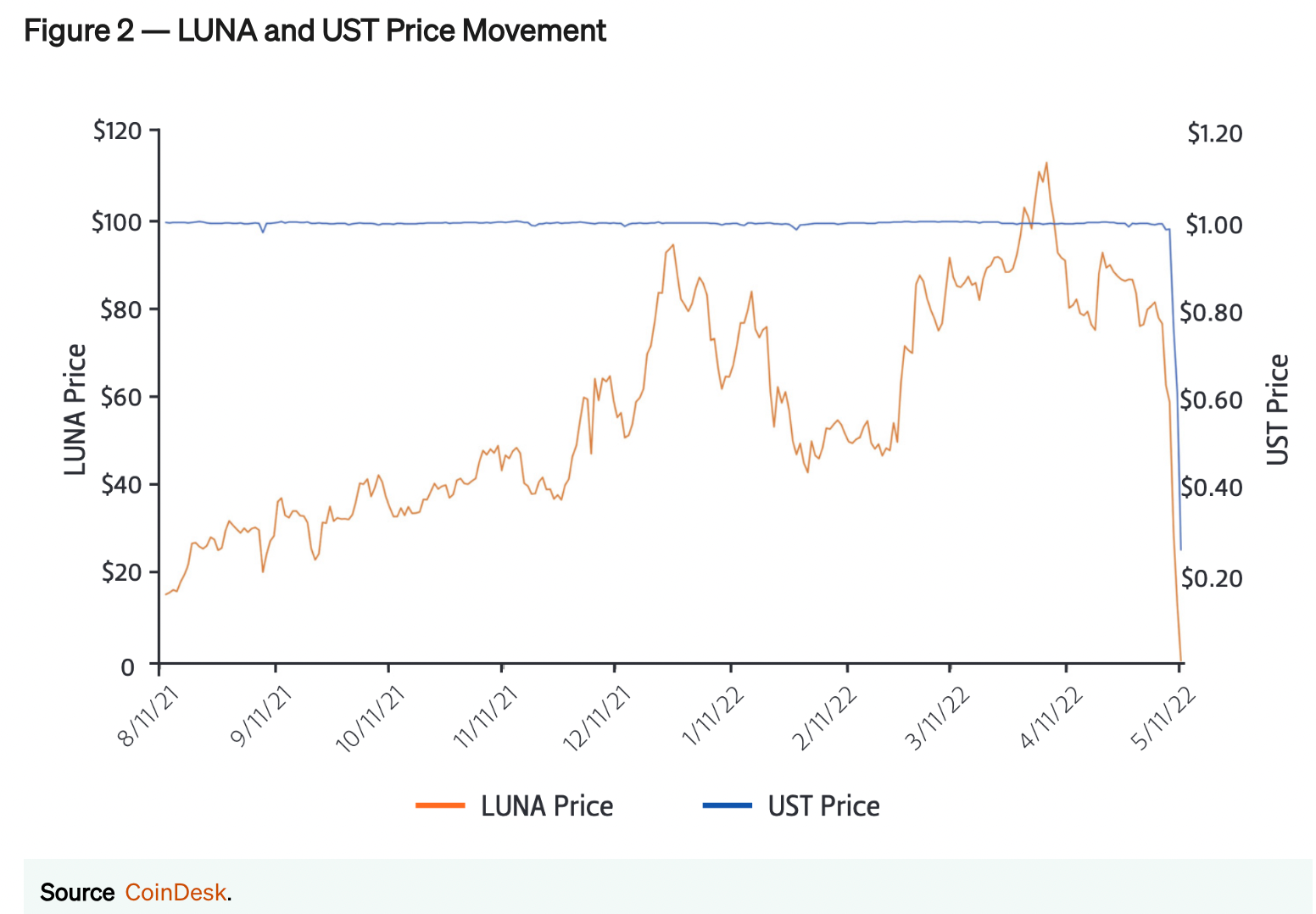

Those fragilities were laid bare in May 2022, when large holders began moving capital out of UST and Anchor, triggering heavy selling pressure on the stablecoin. As UST slipped below its one‑dollar target, the arbitrage mechanism kicked in: UST holders rushed to redeem their coins for Luna, rapidly expanding Luna’s circulating supply.

The dynamic quickly turned vicious. Each wave of redemptions minted more Luna, driving down its price and undermining the very collateral that was supposed to support UST. Within days, Luna’s supply ballooned from billions to trillions of tokens, its price crashed to fractions of a cent, and UST plunged far below its intended peg, effectively wiping out the value of both tokens (7).

The 15‑year sentence and its meaning

Kwon’s 15‑year sentence reflects both the scale of the losses and the court’s view that his misrepresentations were central to the disaster. Victim statements described life savings wiped out and cascading personal hardships, while the judge emphasized that Terra’s collapse ranks among the most damaging frauds ever prosecuted in the digital‑asset space.

The sentence exceeded what Kwon’s lawyers requested and signals that US authorities intend to treat crypto‑related deception much like traditional financial fraud. As part of his plea and related settlements, Kwon faces restrictions on future involvement in the crypto industry and potential transfer abroad once he has served a portion of his US sentence (8).

Lessons for crypto and investors

Terra’s failure has had a lasting impact on how regulators, developers, and investors think about stablecoins and DeFi. Policymakers have pointed to the episode as evidence that complex algorithmic mechanisms and sky‑high yields can obscure risks that resemble classic bank runs, even if they are expressed in code rather than in traditional ledgers.

For investors, the Terra saga underscores several hard lessons: if a yield seems too good to be true, it probably is; stability promises backed by volatile tokens can unravel quickly; and charismatic founders are no substitute for robust, transparent risk controls. Kwon’s conviction and long sentence mark a turning point, showing that even in the still‑evolving world of digital assets, the basic expectations of honesty, disclosure, and accountability still apply and that failing to meet them can carry very real consequences.

References

- Crypto fraudster sentenced for 'epic' $40bn stablecoin crash

- Terra Founder Do Kwon Sentenced to 15 Years in Prison for Fraud

- TerraUSD creator Do Kwon sentenced to 15 years over $40 billion crypto collapse

- Anatomy of a Run: The Terra Luna Crash

- Anatomy of a Run: The Terra Luna Crash

- What is Terra Luna 2.0? Everything you need to know about Terra’s fork

- Crypto mogul Do Kwon sentenced to 15 years in prison for $40 billion stablecoin fraud

- Crypto Magnate Do Kwon Sentenced to 15 Years in Prison

About Netcoins

Established in 2014 in Vancouver, British Columbia, Netcoins is a registered Restricted Dealer with the provincial securities commissions and a registered Money Services Business (MSB) with FINTRAC. The platform operates under BIGG Digital Assets Inc., a publicly traded company listed on the TSX Venture Exchange (TSXV: BIGG), and complies with applicable public company regulatory requirements.

The information provided in the blog posts on this platform is for educational purposes only. It is not intended to be financial advice or a recommendation to buy, sell, or hold any cryptocurrency. Always do your own research and consult with a professional financial advisor before making any investment decisions. Cryptocurrency investments carry a high degree of risk, including the risk of total loss. The blog posts on this platform are not investment advice and do not guarantee any returns. Any action you take based on the information on our platform is strictly at your own risk. The content of our blog posts reflects the authors’ opinions based on their personal experiences and research. However, the rapidly changing and volatile nature of the cryptocurrency market means that the information and opinions presented may quickly become outdated or irrelevant. Always verify the current state of the market before making any decisions.