.png)

Inflation is the decline in purchasing power of money over time and it has resurfaced as a dominant concern across advanced and emerging economies (1). Governments responded to COVID-19 and economic slowdowns with unprecedented fiscal stimulus and monetary expansion, prompting renewed interest in assets that might preserve real value. Bitcoin, with its capped monetary supply and digital nature, is often proposed as one such asset (2).

But what does the empirical evidence say about how Bitcoin actually behaves relative to inflation? Rather than prescribing whether it is or is not a hedge, this article examines the evolving relationship between Bitcoin and inflation pressures, the competing interpretations in research, and the key factors that influence this dynamic.

The Origins of the Inflation-Hedge Narrative

Bitcoin’s fixed supply of 21 million coins is foundational to many arguments about its inflation resistance. Unlike fiat money, which can be expanded through central banking policies, Bitcoin’s issuance schedule is predetermined in code. Early proponents argued that this scarcity inherently shields it from currency debasement. (3)

During periods of aggressive monetary easing 2020–2021, Bitcoin’s price appreciated alongside many assets. Some investors pointed to its growth amid loose policy as evidence that it functioned similarly to traditional inflation hedges like gold. As the narrative matured, commentators and asset managers adopted terms like “digital gold” and “inflation-resistant money” (4).

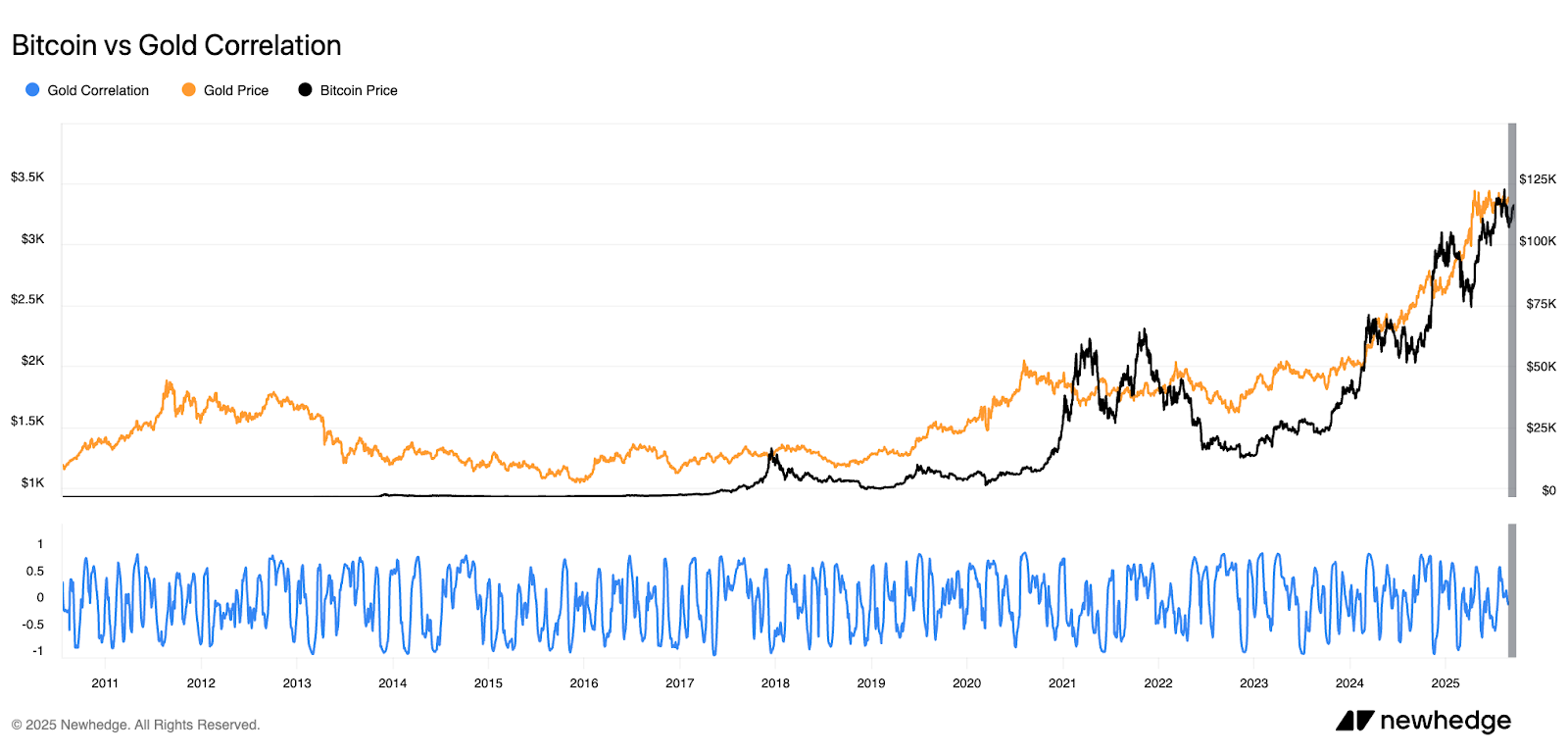

However, critics warned that Bitcoin’s volatility, nascent markets, and sensitivity to macro flows complicate any simple hedge analogy. Fast forward to today with Bitcoin being accepted as a legitimate asset class by traditional finance in the form of ETFs, Strategic Bitcoin reserves, we have seen these steady flows within the last two years bring down Bitcoin's volatility (5).

Evidence from Recent Inflation Cycles

2020–2021: Monetary Expansion & Bitcoin’s Rise

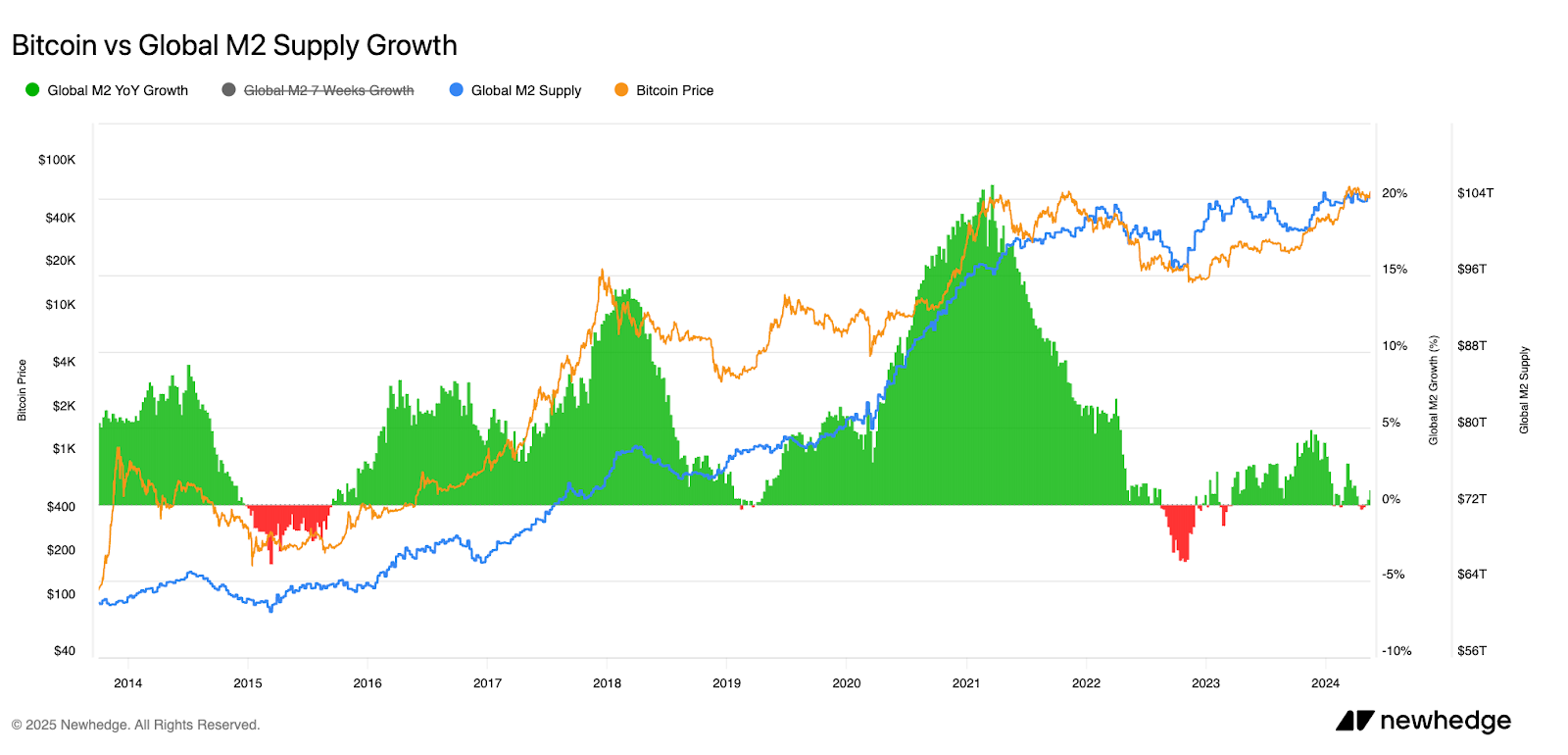

As central banks worldwide flooded liquidity and enacted large stimulus packages, Bitcoin surged. BTC rose in tandem with fears of future price pressures. However, others cautioned that the rally was also supported by speculative demand, momentum, and broad risk-on flows (6). Everyone had stimulus checks coming in during covid time so a natural price appreciation in assets including Bitcoin at a time where we were all more reliant/aware on digital technology made sense. Thus, correlation in that period may reflect confluence, not causation.

2022–2023: Inflation Spikes and Bitcoin Underperformance

Between 2022 and 2023, many economies experienced sharp inflation jumps. During much of this phase, Bitcoin did not exhibit consistent resilience; instead, it underwent deep drawdowns. That undercut arguments claiming that Bitcoin reliably hedges inflation in real time, especially under stress conditions (7).

2024–2025: Cooling Inflation and Rebound in Bitcoin

As inflation has begun normalizing in several advanced economies, Bitcoin has posted periods of strong performance. Some suggest the relationship is less about current inflation and more about expectations, liquidity, and macro regime shifts. Bitcoin’s properties of having a hard fixed supply were strategically implemented with the logic that this characteristic would become more important as fiat debasement in the long run takes place (8).

Institutional Framing

Many now treat Bitcoin less as a pure inflation hedge and more like a high-beta asset. In interviews and commentary, some emphasize its role as a speculative or tactical exposure rather than a stable anchor. Others view it as a potential long-term store of value, but with significant caveats about risk, correlation, and liquidity (9). This divide can be explained because Bitcoin is trying to be a digital version of gold but to become a universal store of value like gold is that takes a long time as gold has been around for centuries while when compared to Bitcoin is in its fancy.

The Role of Market Dynamics

Even when the statistical relationship between Bitcoin and inflation is inconsistent. Narratives can shape flows: when inflation dominates headlines, Bitcoin is often discussed in the same breath as gold, which reinforces its association as a potential hedge.

Importantly, Bitcoin’s price action frequently aligns more closely with liquidity conditions than with realized inflation. Research from the New York Fed finds Bitcoin often unresponsive to monetary announcements, yet sensitive to broader risk appetite and dollar liquidity cycles. In practice, this means Bitcoin’s “inflation hedge” behavior may be less about protecting against prices rising in real time and more about anticipating monetary conditions that often accompany inflation (10).

This complexity has prompted some analysts to argue that Bitcoin functions as a hedge against long-term currency debasement rather than a short-term hedge against CPI fluctuations. The distinction is subtle but significant for institutional framing.

Global Perspectives on Bitcoin and Inflation

The inflation dynamic also differs across geographies:

- Emerging Markets: In countries with weak currencies or high inflation volatility, Bitcoin has sometimes provided a store-of-value alternative. For example, in Turkey and Argentina, trading volumes spike during periods of rapid currency depreciation, reflecting its use as a partial hedge against local monetary instability (11).

- Advanced Economies: In the U.S., Europe, and Japan, Bitcoin behaves less like an inflation hedge and more like a high-risk, high-beta asset. Here, investor flows are tied more to liquidity, regulation, and institutional adoption than to CPI data (12).

This split suggests that Bitcoin’s inflation hedge role may be context-dependent where it is stronger where currency credibility is weakest.

The Future of Bitcoin and Inflation

With inflation pressures easing in advanced economies, the immediate hedge conversation has quieted. Yet Bitcoin’s capped supply ensures the inflation angle will remain central to its identity. Institutional managers are likely to continue monitoring whether Bitcoin offers diversification benefits during future inflationary shocks, even if they stop short of calling it a hedge (13).

At the same time, technological and market structure improvements such as the growth of ETFs, regulated custody solutions, and integration into retirement accounts may strengthen Bitcoin’s appeal as an alternative asset class. These developments do not directly prove its inflation-hedge status, but they deepen its role within the financial system (14).

Ultimately, whether Bitcoin consistently tracks inflation metrics is less important than the fact that it remains framed against inflation in both investor discourse and marketing. The perception of Bitcoin as “sound money” in contrast to fiat currency is likely to endure even if the correlation data tells a more nuanced story.

Resources:

- CNBC, “US inflation hit a 40-year high in 2021” (2022).

- 21Shares, “Why Is Bitcoin a Hedge Against Inflation and Currency Debasement?” (2021).

- Nakamoto, S., Bitcoin: A Peer-to-Peer Electronic Cash System (2008).

- Bitwise, “Unpacking the Intricate Relationship Between Bitcoin and Inflation” (2022).

- T. Conlon et al., “Enduring relief or fleeting respite? Bitcoin as a hedge”, PMC (2023).

- S&P Global, “Are crypto markets correlated with macroeconomic factors?” (2022).

- L. Wagenaar, “Are Cryptocurrencies Good Hedges Against Inflation?”, Univ. of Twente Thesis (2022).

- 21Shares, “Research: Bitcoin’s Scarcity and Fiat Debasement” (2022)

- Federal Reserve Bank of New York, Staff Report No. 1052: The Bitcoin–Macro Disconnect (2023).

- SSRN, “Is Bitcoin a Hedge Against CPI Inflation?” (2022).

- Reuters, “Crypto demand rises in Argentina, Turkey amid inflation” (2023).

- Coindesk, “Institutional adoption reshapes Bitcoin flows” (2024).

- ResearchGate, “Bitcoin as a Hedge Against Inflation in Emerging Markets” (2024).

- CoinDesk, “Institutions eye Bitcoin during inflationary shocks” (2024).

About Netcoins

Established in 2014 in Vancouver, British Columbia, Netcoins is a registered Restricted Dealer with the provincial securities commissions and a registered Money Services Business (MSB) with FINTRAC. The platform operates under BIGG Digital Assets Inc., a publicly traded company listed on the TSX Venture Exchange (TSXV: BIGG), and complies with applicable public company regulatory requirements.

The information provided in the blog posts on this platform is for educational purposes only. It is not intended to be financial advice or a recommendation to buy, sell, or hold any cryptocurrency. Always do your own research and consult with a professional financial advisor before making any investment decisions. Cryptocurrency investments carry a high degree of risk, including the risk of total loss. The blog posts on this platform are not investment advice and do not guarantee any returns. Any action you take based on the information on our platform is strictly at your own risk. The content of our blog posts reflects the authors’ opinions based on their personal experiences and research. However, the rapidly changing and volatile nature of the cryptocurrency market means that the information and opinions presented may quickly become outdated or irrelevant. Always verify the current state of the market before making any decisions.