.png)

Pension funds are among the most important and conservative investors in the global financial system. Together, they manage tens of trillions of dollars in assets, serving as stewards of retirement savings for millions of beneficiaries. Their mandate is clear: preserve and grow capital over decades while meeting long-term obligations.

While hedge funds, endowments, and even corporations have dabbled in Bitcoin, pension funds have been far slower to engage. Their cautious stance reflects not just fiduciary responsibility but also the scrutiny that comes with managing public trust. Yet, as Bitcoin gains legitimacy through regulated products like ETFs and the development of institutional-grade custody, the conversation is shifting. The question is no longer whether Bitcoin is relevant, but whether pension funds can responsibly incorporate it into their framework.

Pension Funds and Their Mandate

Pension funds differ from other institutional investors in key ways. Their purpose is not to maximize returns at all costs but to balance growth with stability. This responsibility shapes their portfolios, which traditionally lean heavily on equities, bonds, and alternative assets like real estate or infrastructure.

Key features of their mandate include:

- Liability-driven investing: Pension funds must meet predictable, long-term payout obligations.

- Risk management: Preservation of capital often outweighs aggressive return-seeking.

- Regulatory oversight: Pension funds are bound by strict fiduciary and legal requirements.

- Public accountability: For public pensions in particular, every allocation is subject to public and political scrutiny.

This cautious DNA explains why pension funds have historically been slow to embrace new asset classes, but also why their eventual participation signals powerful validation.

Why Bitcoin Is on the Radar

Diversification Potential

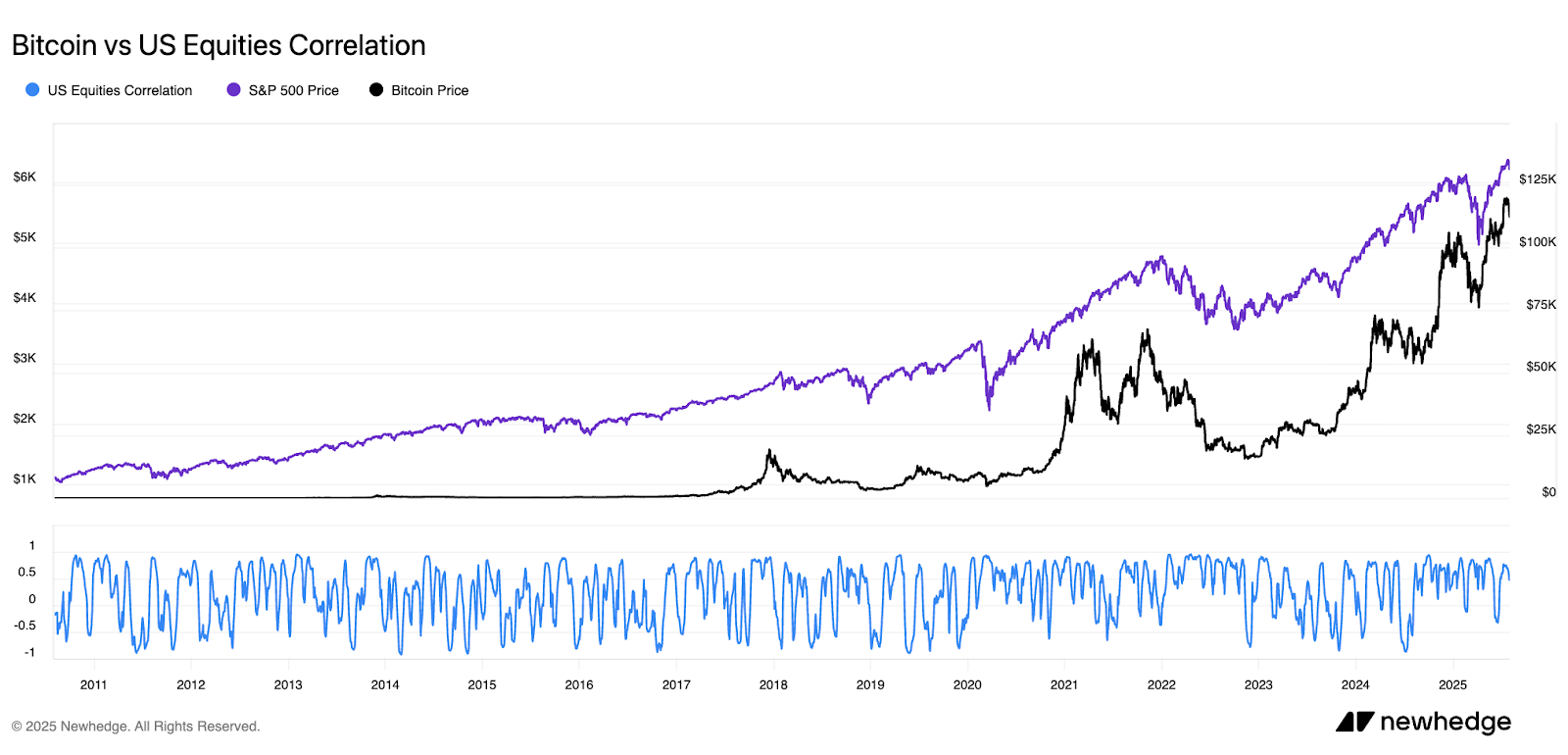

For decades, pension funds have sought assets that behave differently from traditional stocks and bonds. Bitcoin, despite its volatility, has at times demonstrated low correlation with mainstream financial assets. During inflationary periods or currency debasement fears, Bitcoin’s scarcity narrative is slowly gaining an appeal as a potential hedge that resonates with pension fund managers tasked with ensuring resilience across market cycles.

Growing Legitimacy

What was once dismissed as speculative is increasingly entering the financial mainstream. The approval of spot Bitcoin ETFs in Canada (2021) and the U.S. (2024) has provided regulated, transparent vehicles for exposure. Meanwhile, custody solutions offer institutional-grade safeguards, insurance, and compliance frameworks. Together, these developments reduce some of the operational and reputational risks that previously kept pensions on the sidelines.

U.S. 401(k) Crypto Developments under the Trump Administration

In 2025, the Trump administration made several moves that reshaped how retirement plans can view crypto exposure:

- Rescinding prior restrictions: The Department of Labor withdrew 2022 guidance that discouraged employers from offering crypto in 401(k) plans, adopting a neutral stance.

- Executive Order on alternatives: An August 2025 order directed agencies to revise rules to allow alternative assets including cryptocurrencies in participant-directed 401(k)s.

While uncertainties remain around adoption speed and custody structures, these policy shifts signal growing openness to crypto in retirement portfolios, a trend pension funds globally are watching.

Key Challenges for Pension Funds

Volatility and Risk Profile

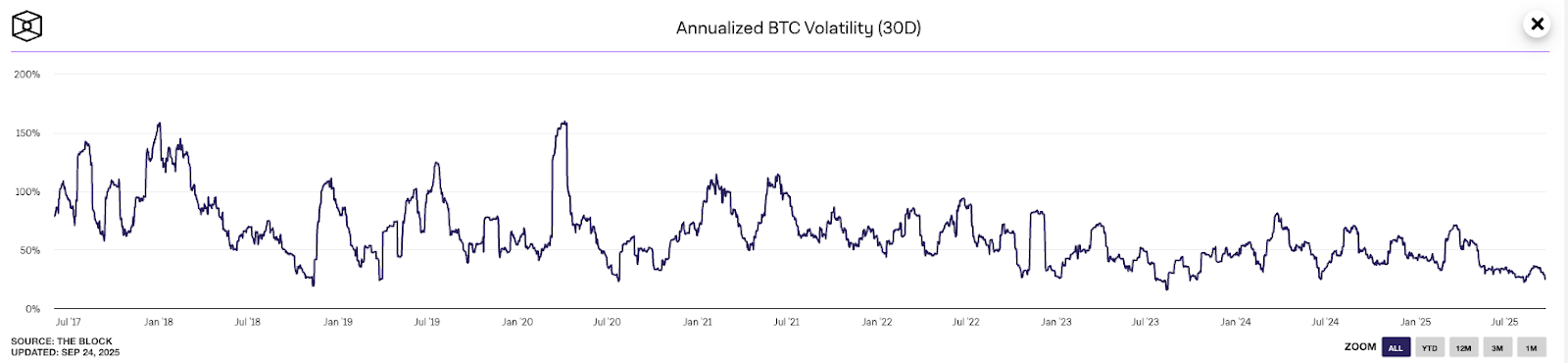

Perhaps the largest hurdle is Bitcoin’s price volatility. While gold or equities experience cycles, Bitcoin’s drawdowns of 50% or more remain outside the comfort zone of most pension trustees. Stress-testing portfolios with even small allocations reveals potential for sharp fluctuations, which can clash with liability-driven models.

Regulatory and Fiduciary Constraints

Pension funds are subject to some of the strictest fiduciary standards in finance. Trustees must be able to demonstrate that any investment is prudent, defensible, and in the best interest of beneficiaries. Although regulation around Bitcoin is improving, the lack of universal standards across jurisdictions creates uncertainty for compliance teams and boards.

Reputation and Optics

Public perception is another challenge. Pension funds operate under intense scrutiny, and a poorly timed Bitcoin investment could be politically damaging. Headlines about losses, even if temporary or offset by gains elsewhere, could undermine trust. This reputational risk often weighs as heavily as the financial analysis itself.

Custody and Governance Considerations

If pension funds are to approach Bitcoin, custody and governance will be central. Unlike traditional securities, Bitcoin is a bearer asset — control of the private keys equals control of the funds. For institutions managing billions, this raises critical questions:

- Custody Solutions: Providers like BitGo and Fireblocks now offer regulated, auditable, and insured solutions, closing a key gap. Their platforms support Cold storage solutions and multi-party computation (MPC) systems that align with fiduciary requirements for checks and balances.

- Insurance and Audits: Custodians are pairing technology with comprehensive insurance policies and third-party audits, essential for reassuring trustees and regulators.

- Governance Frameworks: Pension boards would need detailed policies for allocation size, monitoring, reporting, and rebalancing. These governance steps ensure Bitcoin exposure is integrated responsibly, not treated as a speculative bet.

By embedding Bitcoin into the same risk-controlled frameworks applied to other alternative assets, pension funds can mitigate the operational and fiduciary hurdles.

The Road Ahead

Pension funds are certainly not the first movers in Bitcoin adoption. Their size, conservatism, and public accountability make them deliberate and methodical. Yet when pension funds do eventually allocate to an asset class such as private equity, hedge funds, infrastructure it can offer an additional flow that takes this class to the next level of adoption.

For Bitcoin, the path forward is gradual:

- Continued observation of ETF flows and market maturity.

- Integration through intermediaries (ETFs, listed funds) before any direct exposure.

- Broader adoption as volatility moderates and regulation converges.

The long-term vision is clear: as Bitcoin cements itself as a legitimate asset class, it may eventually join the alternatives sleeve of pension portfolios, alongside real estate, private equity, and commodities. That shift, even at small percentages, would represent billions of dollars in flows and a powerful validation of Bitcoin’s role in global finance.

Pension funds are among the most cautious allocators in the world, and their hesitance toward Bitcoin is unsurprising. But the combination of diversification potential, growing legitimacy, and improving custody solutions means the door is opening slowly, but steadily.

For now, pension funds are observers. Over the coming decade, many may become participants. And when they do, it won’t be a speculative gamble, it will be a carefully governed step in Bitcoin’s march toward global acceptance.

Sources:

Democratizing Assets Into 401K Plans

Employee Retirement Security Act

About Netcoins

Established in 2014 in Vancouver, British Columbia, Netcoins is a registered Restricted Dealer with the provincial securities commissions and a registered Money Services Business (MSB) with FINTRAC. The platform operates under BIGG Digital Assets Inc., a publicly traded company listed on the TSX Venture Exchange (TSXV: BIGG), and complies with applicable public company regulatory requirements.

The information provided in the blog posts on this platform is for educational purposes only. It is not intended to be financial advice or a recommendation to buy, sell, or hold any cryptocurrency. Always do your own research and consult with a professional financial advisor before making any investment decisions. Cryptocurrency investments carry a high degree of risk, including the risk of total loss. The blog posts on this platform are not investment advice and do not guarantee any returns. Any action you take based on the information on our platform is strictly at your own risk. The content of our blog posts reflects the authors’ opinions based on their personal experiences and research. However, the rapidly changing and volatile nature of the cryptocurrency market means that the information and opinions presented may quickly become outdated or irrelevant. Always verify the current state of the market before making any decisions.

.png)