How to Earn Passive Income with Crypto Staking in Canada (2026 Guide)

What if your crypto could earn you money while you sleep? Instead of watching your Bitcoin and Ethereum collect digital dust, staking transforms idle assets into income-generating machines. While Canadian savings accounts offer just 2.25-3% interest (Ratehub.ca, Jan 2026), staking can yield 3-12% annually. But how does it work in Canada, and what does the CRA say about your rewards? Let's break down the simplest path to passive crypto income in 2026.

What is Crypto Staking? (The Simple Explanation)

If you are new to crypto, staking can sound complicated. Think of it like a traditional Guaranteed Investment Certificate (GIC) or a high-interest savings account. You agree to lock up your funds for a period of time, and in return, the network pays you interest.

However, unlike a bank where your money is lent out, in crypto, your "staked" coins are used to help secure the blockchain network. This system is called Proof of Stake (PoS). By validating transactions, you earn a share of the network fees.

Related: Proof of Stake vs. Proof of Work

Why Stake? The Benefits of Passive Yield

Why should you lock up your coins instead of just holding them in a wallet?

1. Compound Interest That Beats Traditional Banking

Canadian banks are offering 2.25-3% on high-interest savings accounts in 2026 (EQ Bank offers around 3%, Neo Financial offers 2.25-2.90% depending on balance). Meanwhile, Ethereum staking yields 3-4%, Solana yields 5-7%, and Polkadot yields 10-13%.

The power of compounding becomes obvious over time. If you stake 10 ETH at 4% APY, you'll earn 0.4 ETH in year one. In year two, you're earning rewards on 10.4 ETH. By year five, you have 12.16 ETH without adding a single dollar - just through compound growth.

2. Network Support (And Why It Matters)

By staking, you're not just earning passive income. You're helping secure a multi-billion dollar network. Validators process transactions, maintain consensus, and prevent attacks. In return, the network pays you a share of transaction fees. It's like being a shareholder who gets dividends, except you're also a critical part of the infrastructure.

3. Inflation Hedge in a Devaluing Dollar

Canada's inflation rate has been volatile in recent years. While traditional savings accounts rarely beat inflation, crypto staking rewards can provide a real return. However, remember: this only works if the coin's price remains stable or appreciates. If ETH crashes 30%, your 4% staking yield won't save you.

How to Stake on Netcoins (Step-by-Step)

Staking on Netcoins is designed to be simple for Canadians. You don't need to run your own validator node or manage complex keys. We handle the technical side for you.

Step 1: Buy or Deposit the Asset

First, you need to own a Proof-of-Stake coin. Popular options available on Netcoins include Ethereum (ETH), Solana (SOL), and Cardano (ADA).

Step 2: Navigate to the 'Stake' Tab

Log in to your Netcoins account and find the "Stake" or "Earn" section in the dashboard.

Step 3: Choose Your Amount and Confirm

Select how much you want to stake.

- Note: Pay attention to the Bonding Period. This is the time it takes for your coins to become active.

- Related: Understanding Bonding and Unbonding Periods

Step 4: Start Earning

Once your stake is active, you will start seeing rewards accumulate in your account automatically.

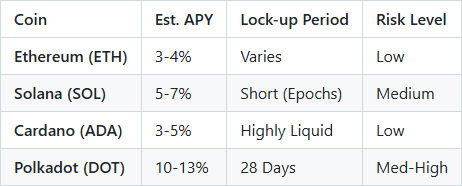

Top Cryptocurrencies to Stake in 2026

Source: StakingRewards.com, Kraken Staking - Data as of January 13, 2026

Note: APYs fluctuate based on network activity and validator performance. Higher yields typically indicate higher risk.

Why the Difference in Returns?

You might wonder why Polkadot offers 10-13% while Ethereum only offers 3-4%. Here's the simple answer: inflation rates and network security models. Polkadot creates new DOT tokens at a faster rate to reward stakers, but this also means more supply entering the market. Ethereum, with a lower inflation rate, offers smaller rewards but potentially better price stability. Think of it like choosing between a high dividend stock with a volatile price versus a stable blue-chip with modest dividends.

The Risks: What You Need to Know

While staking is a powerful wealth-building tool, it comes with risks you need to understand before committing your funds.

1. Slashing Risk (Validator Penalties)

If the network validator handling your stake acts maliciously or experiences extended downtime, a portion of your coins can be "slashed" (permanently removed). For example, on Ethereum, validators can lose up to 1 ETH for serious violations (Ethereum.org).

How Netcoins Protects You: We partner with institutional-grade validators with 99.9% uptime records and robust security infrastructure to minimize this risk.

2. Liquidity Risk (The Unbonding Period)

Most staking protocols require an "unbonding period" when you want to withdraw. During this time (7-28 days depending on the network), your coins are locked and earning zero rewards. Worse, you cannot sell them even if the market crashes.

Real Example: Imagine you stake 100 SOL in January 2026. The market rallies in February, and you want to take profits. You start the unbonding process, which takes 3-4 days. During those days, the market drops 15%. You're forced to watch from the sidelines, unable to react.

3. Market Volatility Outweighs Yield

Crypto markets are notoriously volatile. If you earn 5% in staking rewards but the coin's price drops 25%, you've still lost 20% of your value in CAD terms. Staking rewards don't protect against bear markets. They just soften the blow.

Bottom Line: Only stake coins you plan to hold long-term (1+ years). Never stake your entire emergency fund or money you might need in the next 6 months.

Staking and Taxes in Canada (CRA Rules)

Disclaimer: This is not financial advice. Please consult a tax professional.

Here's the part most Canadians get wrong: staking rewards are taxed differently than capital gains.

How the CRA Treats Staking Rewards

According to the CRA's cryptocurrency guidance, staking rewards are considered income at the time you receive them, not when you sell them (TaxPage.com - Crypto Tax Canada).

Here's what this means in practice:

- Income Tax: The fair market value (in CAD) of the coins you earn is added to your annual income and taxed at your marginal rate (20-50% depending on your province and income bracket).

- Capital Gains Later: When you eventually sell those earned coins, any increase in value from the time you received them is taxed as capital gains (50% of the gain is taxable).

Example:

- You stake 10 ETH and earn 0.4 ETH in rewards over the year

- When you receive that 0.4 ETH, it's worth $1,200 CAD

- You owe income tax on $1,200 (let's say 30% marginal rate = $360)

- A year later, you sell that 0.4 ETH for $1,500 CAD

- You owe capital gains tax on the $300 profit ($1,500 - $1,200)

- Tax owed: 50% × $300 × 30% = $45

Critical Tip: Set aside 25-30% of your staking rewards in a separate account to cover your tax bill in April. Many Canadians get caught off guard by unexpected tax obligations from crypto income.

Deep Dive: Is Crypto Taxed in Canada?

The Bottom Line

Staking is one of the most powerful tools in a crypto investor's arsenal. It transforms your portfolio from a passive collection of assets into an active income generator. By understanding the risks and following the Canadian tax rules, you can safely build wealth over the long term.

Ready to start earning? Log in to Netcoins and Start Staking Today

FAQ Schema

Q: Is crypto staking taxable in Canada? A: Yes, staking rewards are typically considered taxable income by the CRA based on their fair market value at the time of receipt.

Q: Can I lose money staking? A: Yes. While rare, "slashing" can remove a portion of your coins. More commonly, if the coin's price drops significantly, the loss in value may exceed your staking rewards.

Q: Is there a minimum amount to stake on Netcoins? A: Minimums vary by coin but are designed to be accessible for all investors. Check the specific coin's page for current details.

About Netcoins

Established in 2014 in Vancouver, British Columbia, Netcoins is a registered Restricted Dealer with the provincial securities commissions and a registered Money Services Business (MSB) with FINTRAC. The platform operates under BIGG Digital Assets Inc., a publicly traded company listed on the TSX Venture Exchange (TSXV: BIGG), and complies with applicable public company regulatory requirements.

The information provided in the blog posts on this platform is for educational purposes only. It is not intended to be financial advice or a recommendation to buy, sell, or hold any cryptocurrency. Always do your own research and consult with a professional financial advisor before making any investment decisions. Cryptocurrency investments carry a high degree of risk, including the risk of total loss. The blog posts on this platform are not investment advice and do not guarantee any returns. Any action you take based on the information on our platform is strictly at your own risk. The content of our blog posts reflects the authors’ opinions based on their personal experiences and research. However, the rapidly changing and volatile nature of the cryptocurrency market means that the information and opinions presented may quickly become outdated or irrelevant. Always verify the current state of the market before making any decisions.