.png)

A Central Bank Digital Currency (CBDC) is a digital form of a country's fiat currency, issued directly by its central bank and backed by the full faith of the state. Unlike decentralized cryptocurrencies such as Bitcoin or privately issued stablecoins like USDC, a CBDC is a liability of the central bank itself, not a commercial entity (1). The concept emerges at a pivotal moment in the evolution of money. From physical coins and paper notes to electronic bank deposits and mobile payments, money has progressively dematerialized. CBDCs represent the next phase: sovereign digital cash for the internet age. They are being developed in response to the rise of private digital payment systems, fintech platforms, and stablecoins, which have begun to challenge traditional monetary control.

As of 2025, over 130 countries representing 98% of global GDP are exploring CBDCs (2) These initiatives could transform payments, enhance financial inclusion, and strengthen monetary policy transmission. Yet they also raise profound questions about privacy and state surveillance.

This article provides a high-level overview of CBDCs: their core mechanics, motivations, operational models, and most critically their implications for individual privacy in an increasingly digital financial landscape.

What Are CBDCs? Core Concepts

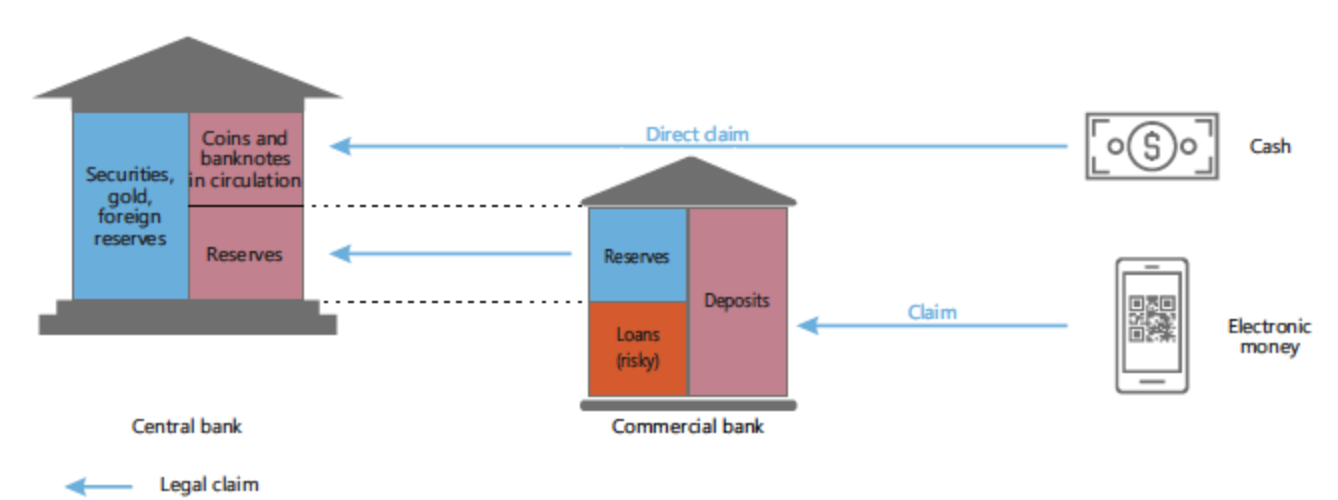

At their essence, CBDCs are digital bearer instruments much like physical cash, they represent a direct claim on the central bank. Key characteristics include:

- Central bank liability: Unlike commercial bank deposits, CBDCs carry no credit risk.

- Digital and programmable: Transactions can be automated, conditional, or time-bound.

- Traceable by design: Every unit can be tracked through the system, unlike anonymous cash.

CBDCs come in two primary forms:

- Retail CBDC: Intended for public use in daily transactions, stored in digital wallets, and used for payments at merchants or peer-to-peer transfers.

- Wholesale CBDC: Restricted to financial institutions for large-value interbank settlements, improving efficiency in money markets.

How CBDCs Work: Technical and Operational Basics

CBDC systems rely on advanced infrastructure to ensure security, scalability, and resilience.

Underlying Technology

Most CBDC projects use a combination of distributed ledger technology (DLT) and conventional centralized databases. Permissioned blockchains accessible only to authorized entities are common, allowing greater control than public blockchains for these use cases (3). Hybrid models tokenize central bank reserves on DLT while maintaining off-chain reconciliation for performance.

Architecture Models

Two dominant designs have emerged:

- Direct Model: The central bank issues CBDC directly to citizens, manages wallets, and processes all transactions. This maximizes control but strains operational capacity.

- Indirect (Two-Tier) Model: The central bank issues CBDC to commercial banks, which then distribute it to the public, handle KYC/AML, and provide customer interfaces. This leverages existing banking infrastructure.

Interoperability

Cross-border functionality is a key goal. The mBridge project led by the BIS Innovation Hub and involving China, Hong Kong, Thailand, and the UAE demonstrates real-time, multi-CBDC settlements on a shared DLT platform (4).

Security Features

CBDCs incorporate:

- End-to-end encryption

- Offline payment capabilities (via secure elements in devices)

- Digital signatures and anti-counterfeiting protocols

- Resilience against quantum computing threats (in forward-looking designs)

Motivations and Benefits

Central banks pursue CBDCs for four main reasons:

Efficiency and Cost Reduction

Digital issuance eliminates cash printing, transportation, and storage costs. Domestic payments settle instantly, and cross-border transfers could bypass correspondent banking networks, reducing fees from 6.5% to under 1% in some corridors (5).

Financial Inclusion

Over 1.4 billion adults remain unbanked (6). A retail CBDC accessible via basic mobile phones could bring them into the formal economy without requiring a traditional bank account.

Monetary Policy Enhancement

CBDCs enable direct policy transmission. Central banks could:

- Apply negative interest rates without cash hoarding

- Deliver targeted stimulus to specific groups

- Gather real-time economic data for better forecasting

Privacy and Surveillance Considerations

The most contentious aspect of CBDCs is their impact on financial privacy.

Traceability vs. Anonymity

Physical cash is anonymous: once handed over, no record links payer to payee. CBDCs, by contrast, are inherently traceable. Every transaction generates a digital footprint, potentially linked to a verified identity (7). This creates the risk of comprehensive financial profiling, governments could monitor spending patterns, political donations, or personal habits in real time.

Surveillance Implications

In a CBDC system:

- The state gains panoptic visibility into economic behavior.

- Data could integrate with social credit systems, as piloted in China’s digital yuan (8).

- Law enforcement could freeze or reverse transactions remotely.

Even in democracies, mission creep is a concern: emergency powers during crises could normalize surveillance.

Mitigation Strategies

Privacy can be preserved through technology and law:

- Zero-knowledge proofs: Prove a transaction occurred without revealing details

- Selective disclosure: Share only necessary data with authorities

- Decentralized identity systems: Users control their data

- Independent audits and sunset clauses on data retention

The European Central Bank, for instance, has prioritized "privacy by design" in its digital euro investigations, exploring offline functionality and anonymized small payments (9).

Fintechs and payment providers will likely build user-friendly wallets and interfaces. Partnerships with Visa, Mastercard, and mobile operators could drive adoption if privacy is not sacrificed for convenience.

CBDCs represent a profound evolution in money: sovereign, digital, and programmable. They promise faster payments, greater inclusion, and more effective policy tools. But they also risk transforming money from a neutral medium of exchange into a tool of control.

The central challenge is design. Will CBDCs replicate the anonymity of cash in digital form, or will they become the ultimate surveillance currency? Policymakers must embed privacy by design, enforce strict data minimization, and ensure independent oversight. Citizens, in turn, must demand transparency and accountability.

The choice is not between innovation and privacy but whether we can achieve both.

Recourses

- III. Artificial intelligence and the economy: implications for central banks

- Annual Economic Report 2025

- Project mBridge: connecting economies through CBDC

- Project mBridge: connecting economies through CBDC

- Remittance Prices Worldwide

- World Bank Group - Financial Inclusion

- Modular Design of Secure Group Messaging Protocols and the Security of MLS

- Atlantic Council

- Some lessons for crisis management from recent bank failures

About Netcoins

Established in 2014 in Vancouver, British Columbia, Netcoins is a registered Restricted Dealer with the provincial securities commissions and a registered Money Services Business (MSB) with FINTRAC. The platform operates under BIGG Digital Assets Inc., a publicly traded company listed on the TSX Venture Exchange (TSXV: BIGG), and complies with applicable public company regulatory requirements.

The information provided in the blog posts on this platform is for educational purposes only. It is not intended to be financial advice or a recommendation to buy, sell, or hold any cryptocurrency. Always do your own research and consult with a professional financial advisor before making any investment decisions. Cryptocurrency investments carry a high degree of risk, including the risk of total loss. The blog posts on this platform are not investment advice and do not guarantee any returns. Any action you take based on the information on our platform is strictly at your own risk. The content of our blog posts reflects the authors’ opinions based on their personal experiences and research. However, the rapidly changing and volatile nature of the cryptocurrency market means that the information and opinions presented may quickly become outdated or irrelevant. Always verify the current state of the market before making any decisions.